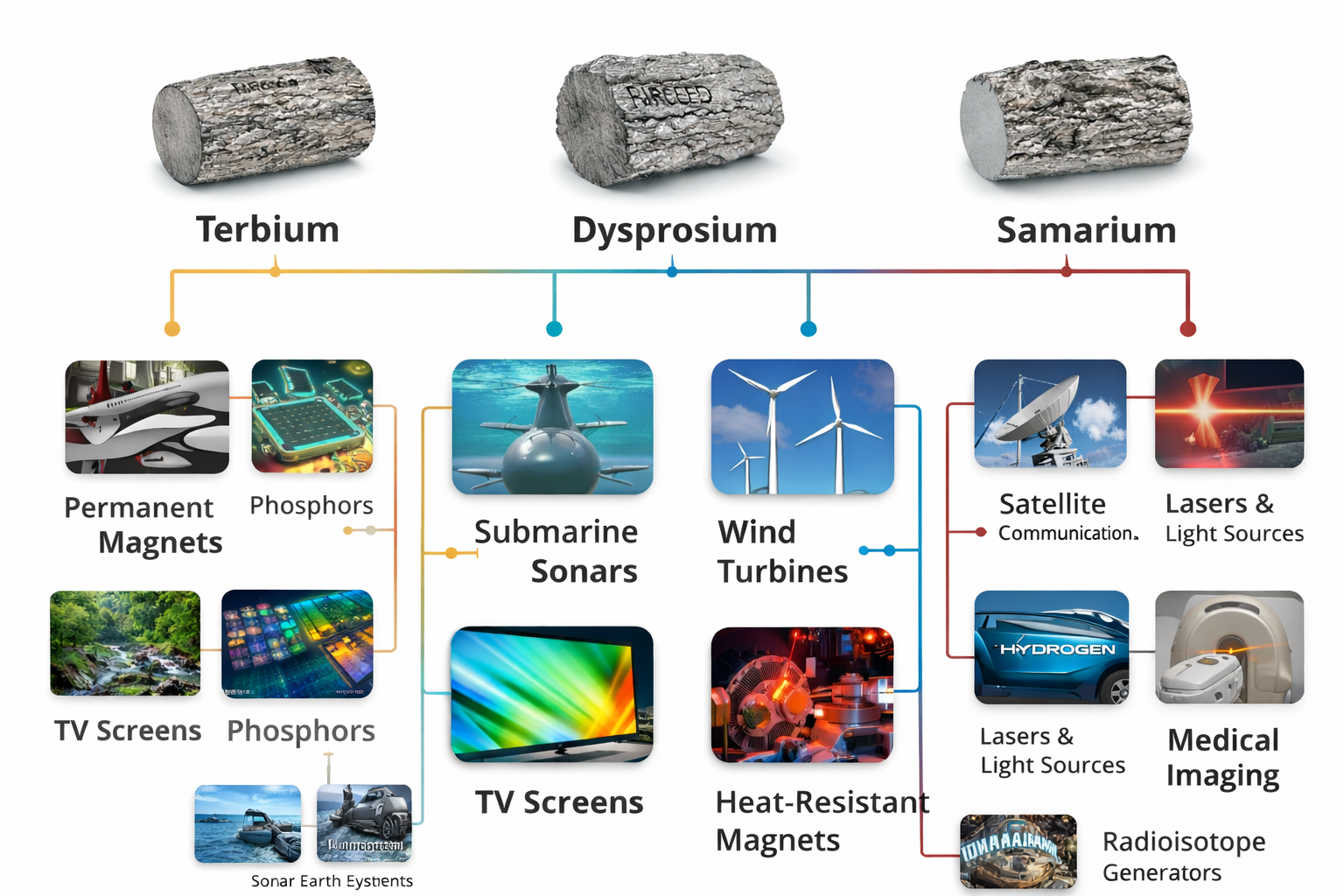

Europe's Raw Materials Dilemma: Between China, Trump, and Russia's Rare Earths

Last year, Ursula von der Leyen brought a small magnet with her to the G7 summit in Canada. A permanent magnet containing rare earths, to be precise. What made it special, according to the President of the European Commission, was that “it was manufactured in Estonia by a Canadian company using Australian raw materials,” von der Leyen told her attentive audience.

The Canadian company in question is, of course, Neo Performance Materials, which emerged from the bankruptcy estate of Molycorp, the former operator of the U.S. rare earth mine at Mountain Pass. In Estonia, Neo operates not only its new permanent rare earth magnet factory but also, dating back to the Molycorp era, one of the few rare earth refining and separation facilities outside China. For the EU, it is a strategic asset that could help reduce its dependence on China for rare earths.

What von der Leyen did not mention is that Estonia's largest supplier of rare earth compounds by far has, for many years, been Russia. According to the EU trade database, the Baltic nation imported more than 3,700 tonnes from its much-maligned neighbour in 2024. In 2025, that figure rose to nearly 4,000 tonnes. Imports from Australia, by contrast, amounted to just three kilograms in 2025 and nothing at all in previous years. Even if these raw materials did not necessarily end up in Neo’s magnet production, the trade relationship nevertheless warrants closer examination.

Estonia as a Hub for Russian Rare Earths

Last year, Estonia exported 2,265 tonnes of mixed rare earth oxides to the United States, 1,000 tonnes to Japan, and 330 tonnes to Switzerland. Germany received 400 tonnes of mixed rare earth oxides from Estonia, whose Russian origin appears highly likely given the trade statistics. Could Estonia, which publicly maintains one of the toughest stances toward Russia, actually be serving as a trading hub for Russian rare earths?

Historically, Estonia remains shaped by Soviet industrial structures. Under Stalin, the oil shale industry in Sillamäe was converted for uranium enrichment. As a result, the town disappeared from maps and became one of the Soviet Union’s secret closed cities. Native Estonians were deported, expelled, or murdered. Stalin filled the resulting labour gap, among others, with Russian Gulag prisoners. To this day, ethnic Russians account for 85 percent of the town’s population. The demographic balance is likely similar across the wider Ida-Viru region.

From the 1970s onward, Sillamäe also produced rare earths and other specialty metals such as tantalum and niobium. In Russia itself, little remains today of the rare earth value chain. Following the collapse of the Soviet Union, key facilities were lost. Those facilities are now located in Kazakhstan and, notably, Estonia.

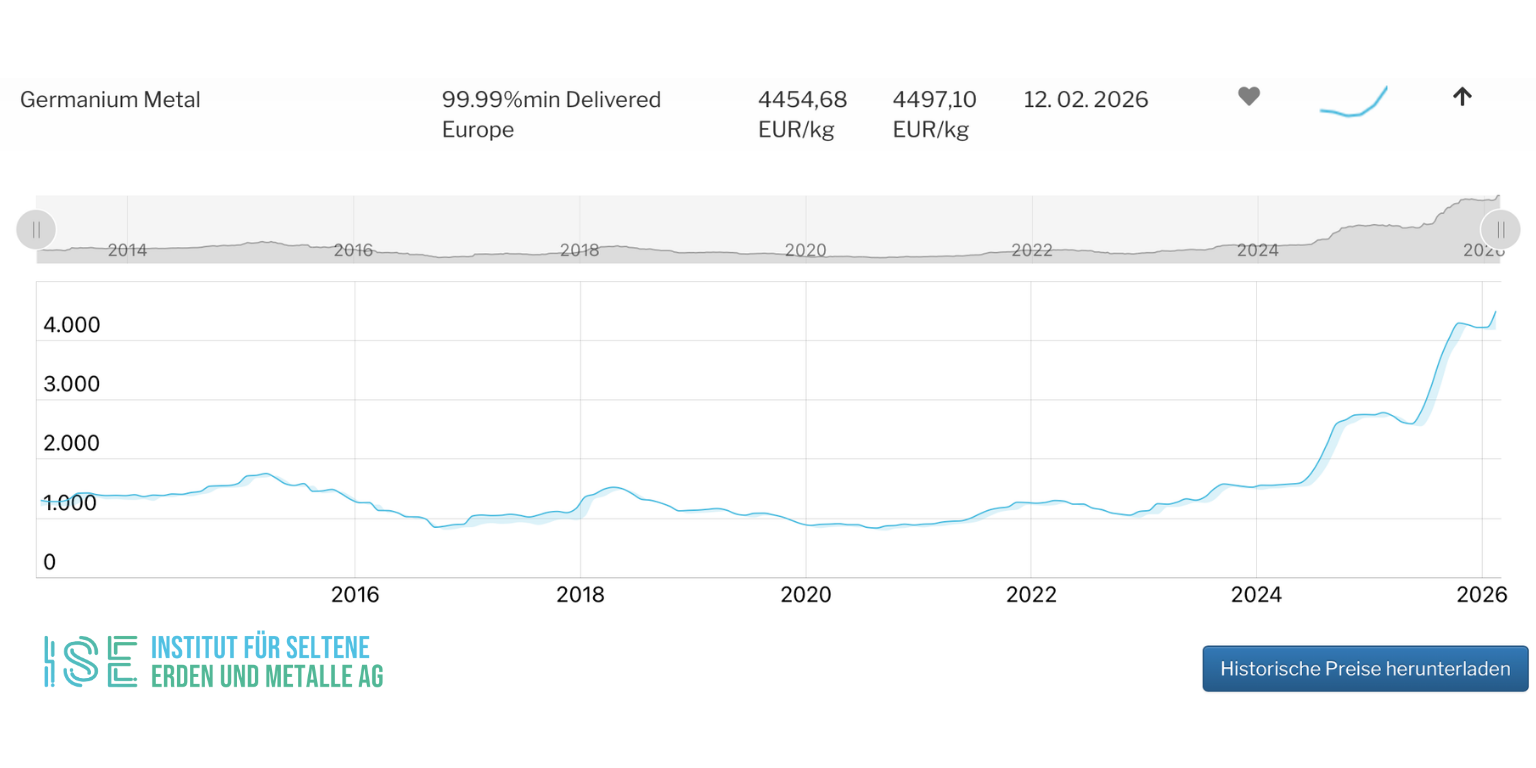

The Neo Silmet facility in Sillamäe, Estonia, is one of the few rare earth processing sites outside China and plays an important role in Western supply chains.

Europe's Raw Materials Dilemma: Between China, Trump, and Russia's Rare Earths

Europe's raw materials transition is colliding with global power interests — and revealing surprising dependencies on Russia.

Last year, Ursula von der Leyen brought a small magnet with her to the G7 summit in Canada. A permanent magnet containing rare earths, to be precise. What made it special, according to the President of the European Commission: “It was manufactured in Estonia by a Canadian company using Australian raw materials,” von der Leyen told her attentive audience.

The Canadian company in question is, of course, Neo Performance Materials, which emerged from the bankruptcy estate of Molycorp, the former operator of the U.S. rare earth mine at Mountain Pass. In Estonia, Neo operates not only its new permanent rare earth magnet factory but also, dating back to the Molycorp era, one of the few rare earth refining and separation facilities outside China. For the EU, it is a strategic asset that could help reduce its dependence on China for rare earths.

What von der Leyen did not mention: Estonia’s largest supplier of rare earth compounds by far has for many years been Russia. According to the EU trade database, the Baltic nation imported more than 3,700 tonnes from its much-maligned neighbour in 2024. In 2025, that figure rose to nearly 4,000 tonnes. Imports from Australia, by contrast, amounted to just three kilograms in 2025 and nothing at all in previous years. Even if these raw materials did not necessarily end up in Neo’s magnet production, these trade relationships nevertheless warrant closer scrutiny.

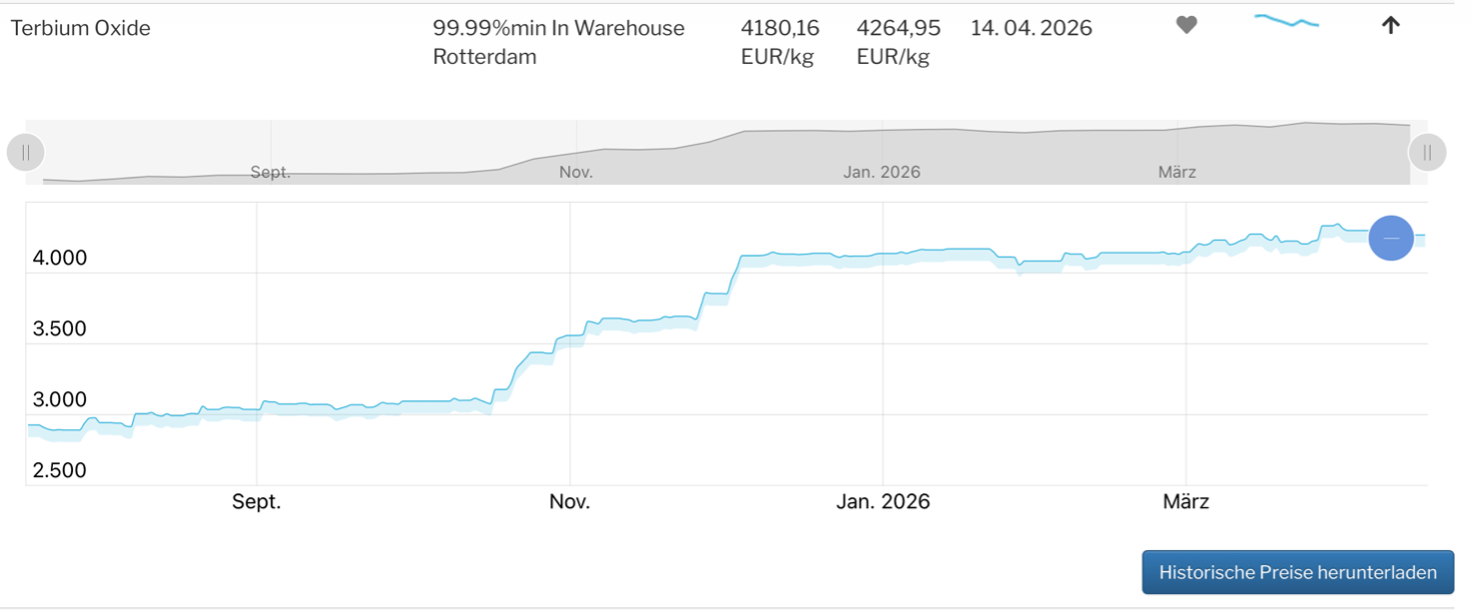

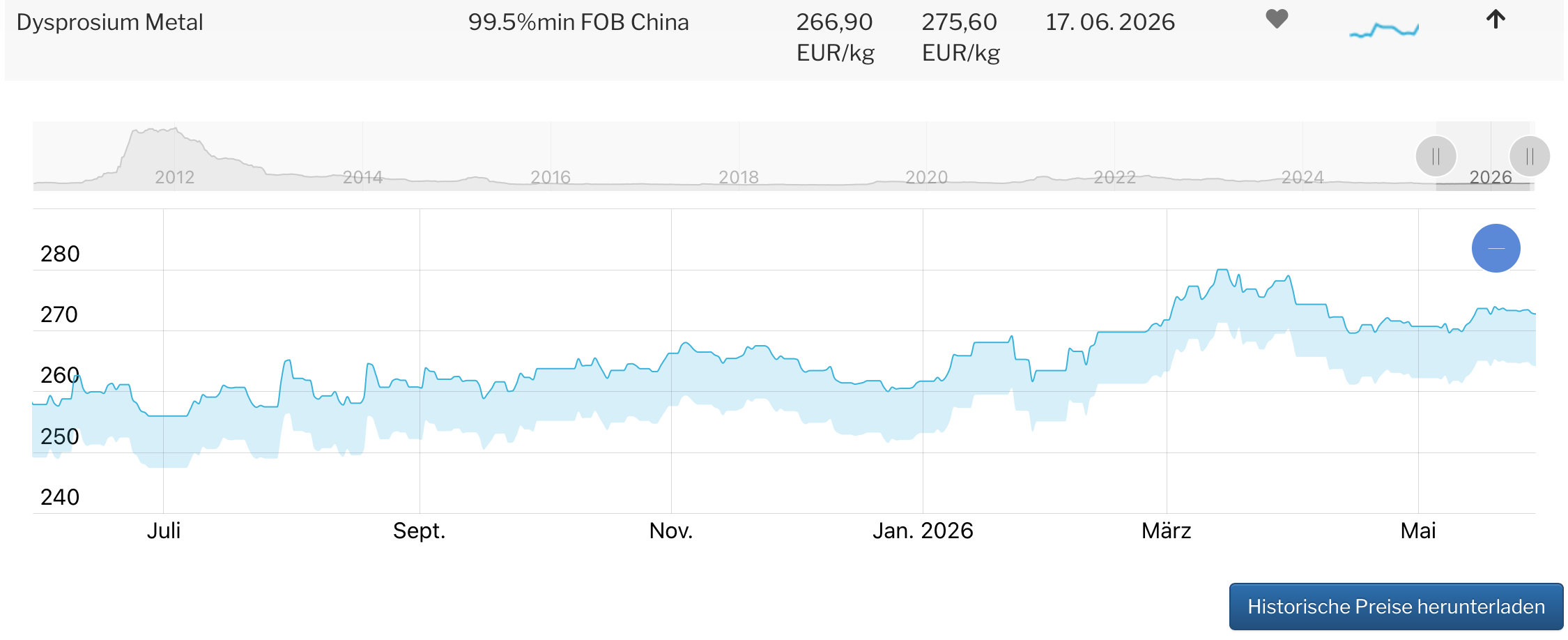

Chart: Dysprosium Metal 99.5% min FOB China, Quelle ISE-AG.COM

Estonia as a Hub for Russian Rare Earths

Last year, Estonia exported 2,265 tonnes of mixed rare earth oxides to the United States, 1,000 tonnes to Japan, and 330 tonnes to Switzerland. Germany received 400 tonnes of mixed rare earth oxides from Estonia, whose Russian origin appears highly likely given the trade statistics. Could Estonia, which publicly maintains one of the toughest stances toward Russia, actually be serving as a trading hub for Russian rare earths? Chart: Dysprosium Metal 99.5% min FOB China, Quelle ISE-AG.COM

Historically, Estonia remains shaped by Soviet industrial structures. Under Stalin, the oil shale industry in Sillamäe was repurposed for uranium enrichment. As a result, the town disappeared from maps and became one of the Soviet Union’s secret closed cities. Native Estonians were deported, expelled, or murdered. Stalin filled the resulting labour gap, among others, with Russian Gulag prisoners. To this day, ethnic Russians account for 85 percent of the town’s population. The demographic balance is likely similar across the wider Ida-Viru region.

From the 1970s onward, Sillamäe also produced rare earths and other specialty metals such as tantalum and niobium. In Russia itself, little remains today of the rare earth value chain. Following the collapse of the Soviet Union, key facilities were lost. Those facilities are now located in Kazakhstan and, notably, Estonia.

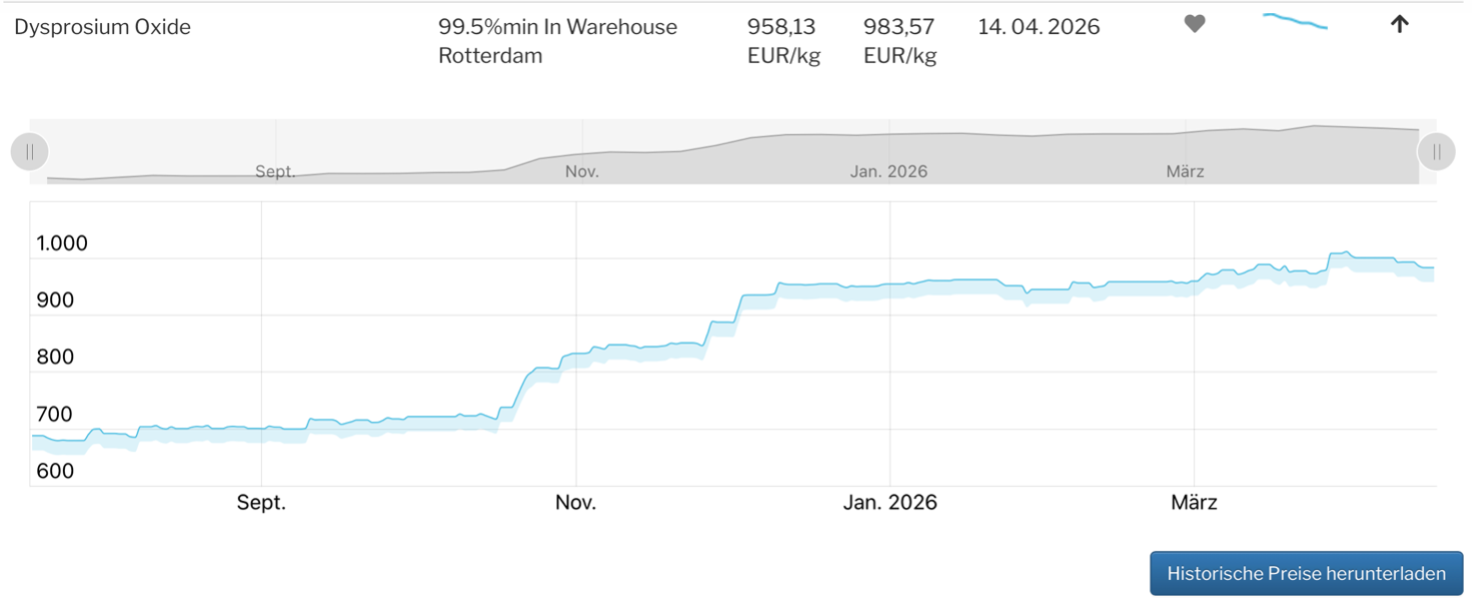

Chart: Neodym Metal 99% min FOB China, Quelle ISE-AG.COM

Tomtor: The Treasure of Siberia

Before the conflict in Ukraine, Russia planned to invest $1.5 billion, according to Reuters, in order to become the world's second-largest producer of rare earths after China by 2030 and secure a global market share of up to 12 percent. The centerpiece of this strategy is the Tomtor deposit in eastern Siberia, which contains exceptionally high metal grades. As of the end of 2019, ore reserves were estimated at more than 11 million tonnes, with grades of nearly 15 percent rare earth oxide and 6 percent niobium oxide. This makes Tomtor one of the richest known rare earth deposits in the world. Chart: Neodym Metal 99% min FOB China, Quelle ISE-AG.COM

Putin had already been pushing for the development of the deposit in 2014. Yet the license holder, ThreeArc Mining, which was controlled through the IST Group by businessman Alexander Nesis, failed to launch production over the course of a decade. Putin publicly complained about the delay and called for the project to be accelerated. “This is a strategically important resource that the state needs now,” the Russian president said during a Kremlin meeting in late 2024. A year ago, state-owned oil giant Rosneft finally took over the project.

Yet the immense challenge remains. The deposit is located in one of the most remote and coldest regions on Earth, where temperatures can drop to minus 60 degrees Celsius. Due to the lack of roads, the area can only be reached by helicopter. ThreeArc Mining originally planned to transport the ore several thousand kilometers to Rosatom’s planned hydrometallurgical processing facility in Krasnokamensk in southeastern Siberia, near the Chinese border. The ore can only be transported during winter via frozen rivers. According to geological consultancy SRK, however, the exceptionally high grades justify the logistical and technical effort.

Another challenge is the complex geology of the Tomtor ore. Due to its fine-grained structure, it cannot be beneficiated using conventional methods, according to a report by S&P Global. Russia currently lacks the necessary technologies. Rosneft, the new operator, could send the ore to Solikamsk, provided that Rosatom’s Solikamsk Magnesium Plant (SMZ) builds a dedicated processing facility specifically for Tomtor ore, an analyst told S&P Global. More likely, however, is that the ore will be shipped to China. The unnamed analyst expects pilot production to begin as early as 2027.

Technology: China Keeps Russia at Arm’s Length

Russia needs rare earths primarily for its petrochemical industry, a cornerstone of the country’s revenues. Growing demand is also coming from Russia’s defense sector. Yet 98 percent of Russia’s rare earth requirements are currently supplied by China. In search of technology, the Kremlin turned to Beijing. After all, both countries have proclaimed a “friendship without limits.” However, when it comes to rare earths, the relationship appears less intimate. As of November 2025, negotiations had made no progress, according to Deputy Prime Minister Denis Manturov.

Manturov was also unable to present any substantial achievements at the St. Petersburg International Economic Forum earlier this month. The only positive development has been the publication of a joint study by Russian and Chinese academics concluding that the most promising model for Sino-Russian cooperation would be a consortium structure similar to the Yamal LNG and Power of Siberia projects.

“This format would allow Russia to attract investment and technology, while enabling China to secure access to new sources of raw materials and strengthen its presence in the Arctic,” write Kou Jingna of Taiyuan University of Technology, along with Alexei Cherepovitsin and Irina Dorozhkina of Saint Petersburg Mining University.

China strictly protects its rare earth extraction and processing technologies and subjects them to restrictive export controls. These restrictions apparently apply even to close partners. At the same time, Beijing is seeking greater access to the Arctic. In 2018, China unveiled its “Polar Silk Road” strategy, under which it described itself as a “near-Arctic state.” Since then, China has steadily expanded its access and presence in the region. Russia is an important partner in these ambitions and could potentially use Arctic access as a bargaining chip in exchange for technological know-how.

Meanwhile, pressure and uncertainty are growing in the West. On November 10, additional regulations concerning rare earths as dual-use goods will come into force. If Beijing fully enforces these measures, they could have devastating consequences for the global economy. The United States, in particular, is mobilizing all available resources to reduce its dependence on Chinese rare earths. Putin is well aware of this leverage. During negotiations over a possible peace settlement for Ukraine, Russian envoys reportedly used a “rare earth partnership” as a bargaining tool.

In early 2025, while the United States was negotiating a minerals agreement with Ukraine that also involved rare earths, Putin publicly offered Washington a joint development of Russian rare earth deposits.

“We undoubtedly possess — and I want to emphasize this — significantly more resources of this kind than Ukraine,” the Russian president said in an interview with state television.

Trump subsequently stated in Washington that efforts were underway to reach economic agreements with Russia.

“They have a lot of things that we would like to have, and we'll see,” the U.S. president said.

Yet here, too, the rhetoric has so far failed to translate into concrete action. Russia is now turning to alternative partners, including India. Speaking at the Raremet-2026 Congress in Moscow at the end of May, Sarada Bhushan Mohanty, head of India Rare Earth Limited, expressed interest in the Tomtor deposit, according to Interfax. India aims to produce 6,000 tonnes of magnets annually and will require corresponding raw materials, said Deependra Singh, chairman of the Rare Earth Association of India, who pointed to the historically strong relationship between India and Russia.

The “Siberianization” of Russia

According to Konstantin Ivanovskikh of Rosatom’s Giredmet Institute, Indian investors have also expressed interest in the planned Angara-Yenisei Cluster in Siberia, a project whose implementation Putin has entrusted to his close ally and former Defense Minister Sergei Shoigu. The cluster is to be developed across the Krasnoyarsk region, Irkutsk Oblast, Khakassia, and Shoigu’s home region of Tuva, with the aim of utilizing Siberia’s natural resources for the country’s sustainable and innovative development.

The Kremlin and Russian media refer to this strategy as the “Siberianization” of Russia, reflecting a shift away from the West and toward the Far East. It also entails the development of a region that remains relatively underdeveloped in terms of infrastructure and industry.

The $9 billion project aims to create an ecosystem for the extraction and processing of rare metals and rare earths, as well as the development of advanced materials, microelectronics, energy solutions, and artificial intelligence systems. However, the ambitious undertaking is unlikely to succeed without foreign capital.

According to political scientist Kirill Shamiev of the European Council on Foreign Relations, Russia appears to believe that Europe’s dependence on China, weak economic growth prospects, and Trump’s confrontational stance toward the European Union will ultimately persuade European governments to engage with the proposal.

Some Europeans, Shamiev warns, may indeed be tempted to present economic agreements with Moscow as a “European solution” to the war in Ukraine or as a safeguard against American pressure and dependence on China.

Europe therefore needs a coherent strategy to resist such an offer, Shamiev argues.

Institute for Rare Earths and Metals

Arndt Uhlendorff – June 2026

ISE AG, Institut für seltene Erden und Metalle AG

- Hits: 331