Metal prices as an indicator of political change worldwide

Arndt Uhlendorff, CEO of the Institute for Rare Earths and Metals AG, explains why it is so important to track and analyse the fluctuations in metal prices

BY OBSERVING fluctuations in metal prices and understanding patterns established over decades and centuries, we can gain insights into global events, anticipate future developments, and make informed decisions – whether to buy, sell, and at what price.

Metal prices are highly volatile during times of anticipated or ongoing military conflicts. These fluctuations result from a combination of economic, geopolitical, and psychological factors.

Gold plays a pivotal role during periods of economic instability or geopolitical tension. Nations often increase their gold reserves because it serves as a ‘safe haven’ asset. Gold is not tied to financial systems (e.g., SWIFT), enabling countries to bypass international sanctions. During wars or major conflicts, gold can be used to pay for imported weapons, food, and other essential goods.

During world wars, many countries expanded their gold reserves, understanding that their currencies might

lose value. For example, Germany and the United States heavily relied on gold during the First and Second World Wars to purchase resources.

In recent years, nations like Russia, China, and India have significantly increased their gold reserves. This move is linked to diversifying reserves and preparing for potential economic upheavals.

During global crises such as the COVID-19 pandemic or escalating geopolitical tensions, gold prices reached record highs, reaffirming its status as a ‘safe harbour.’ Monitoring gold prices can thus be a key to predicting geopolitical shifts and the prices of other metals and metal products.

For example, sanctions imposed on Russia in 2022 after the outbreak of the war with Ukraine led to a sharp increase in palladium and nickel prices, as Russia is one of the largest producers of these metals.

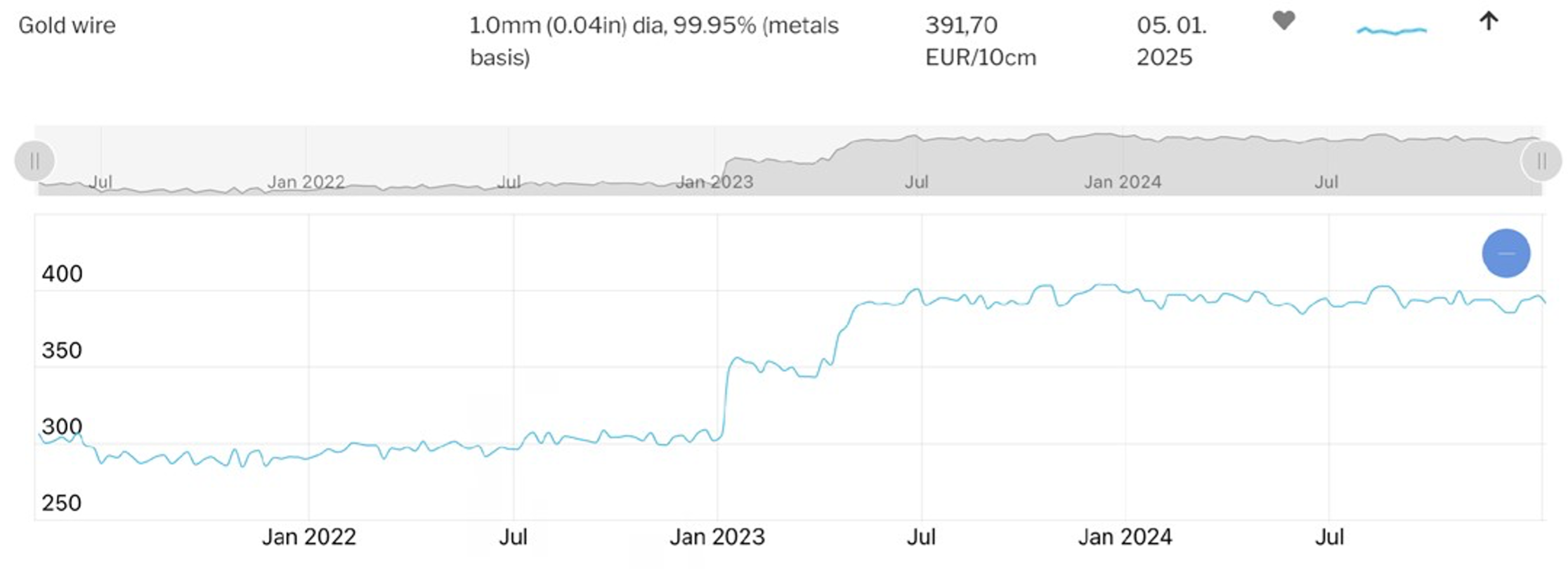

The rise in gold wire prices as an example of a reaction to the launch and active development of artificial intelligence (AI) technologies

The sharp rise in the price of gold wire in 2023 illustrates how technological innovations, such as the development of artificial intelligence (AI) technologies, can drive demand for specific metal products used in microelectronics and semiconductors.

Gold wire prices remained relatively stable at around €300 per 10cm until 2023, but the large-scale production of chips and high-performance computing systems that use gold (e.g., in conductors and microcircuits) caused a significant price surge, stabilising at around €400 per 10cm.

The rise in gold wire prices due to AI technology development

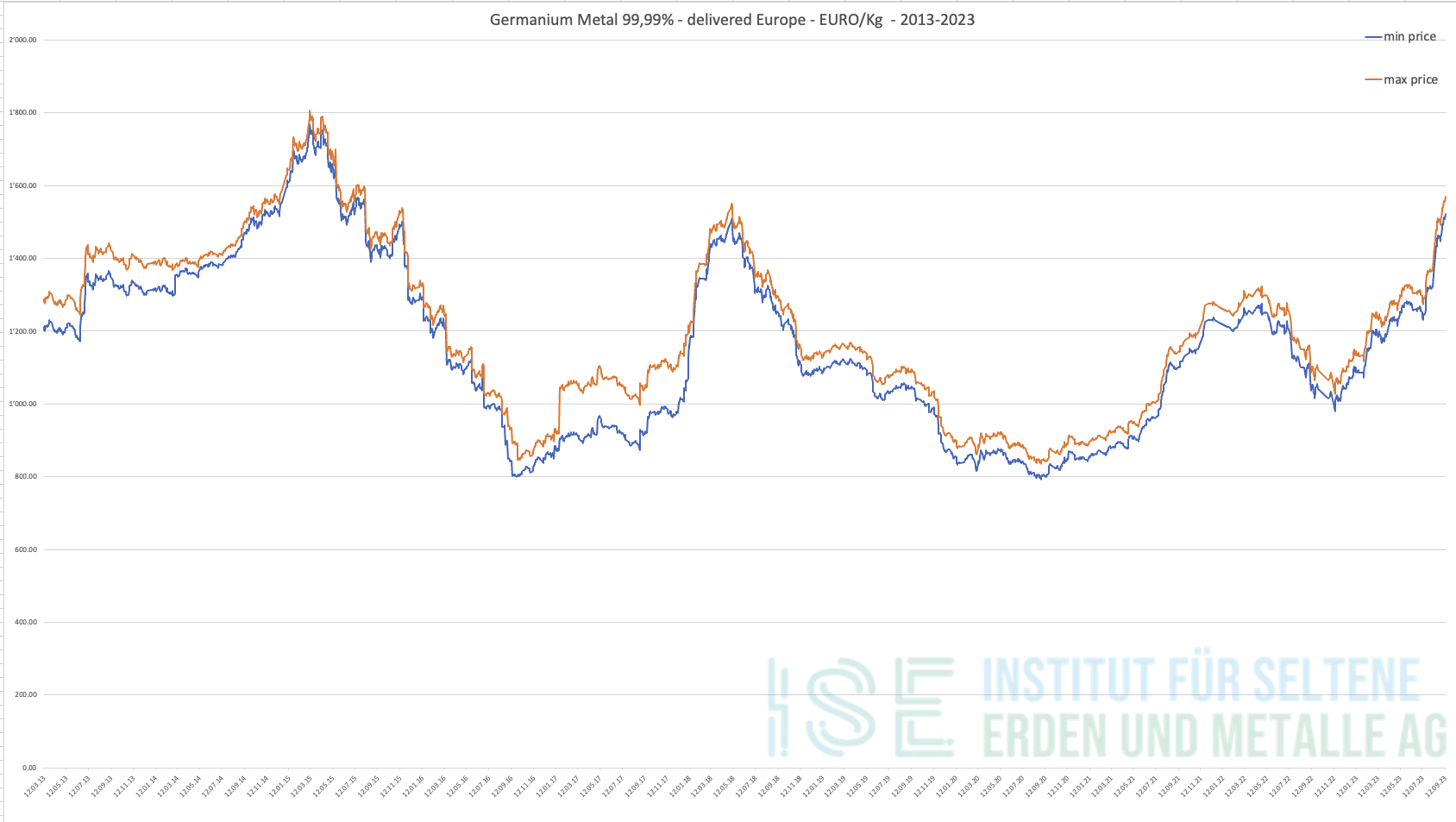

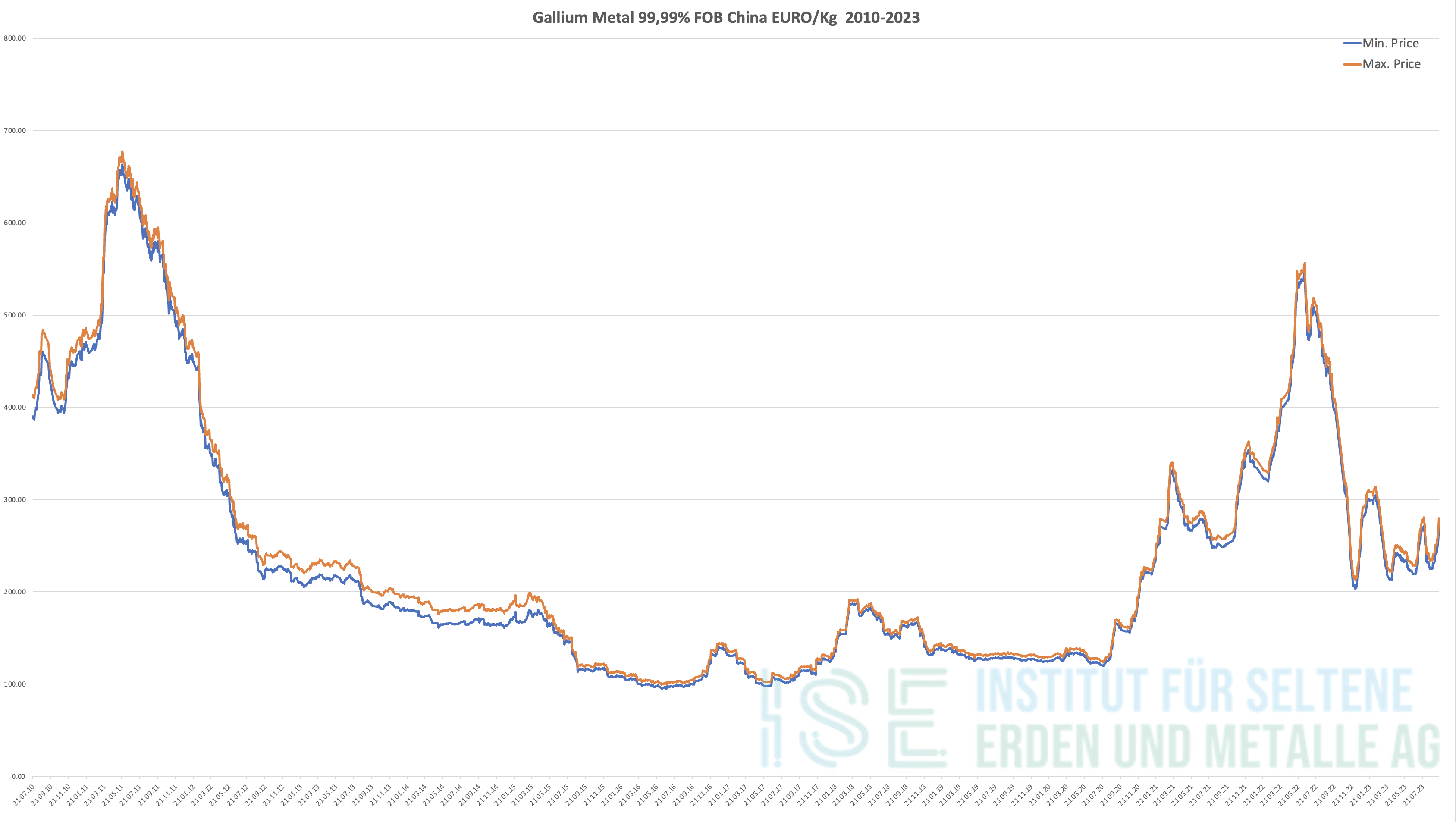

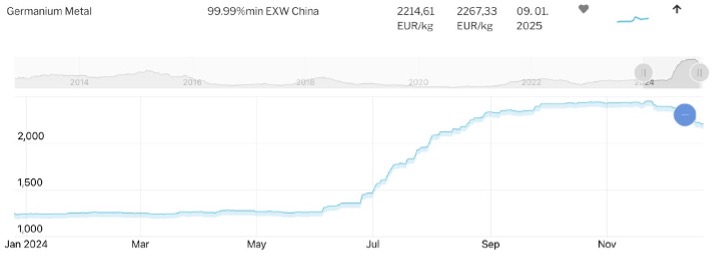

Another recent example of political actions impacting the global market is the sharp rise in prices for gallium, germanium, and antimony in the summer of last year. This coincided with China’s announcement of restrictions on the export of rare metals like gallium and germanium, essential for US microelectronics production. These restrictions were a response to US actions aimed at curbing China’s microelectronics industry.

The US ban on transferring cutting-edge technologies and next-generation microchips to China set the country back several years in AI development, including military AI technologies. With China controlling over 80% of global germanium production and US government gallium reserves running low, these measures had farreaching consequences.

Following stricter restrictions, China nearly ceased exporting gallium and germanium to the US, causing a sharp price increase: gallium prices rose by 80%, and germanium prices doubled. According to estimates by the U.S. Geological Survey, a total export ban on these materials could cost the US economy $3.4bn. While Washington is seeking to diversify supply chains, a quick resolution seems unlikely.

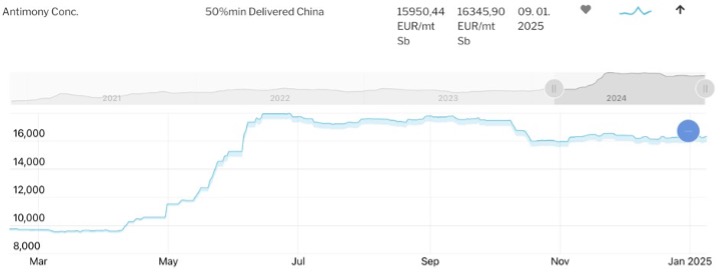

The impact of Chinese government restrictions on antimony exports

In addition to gallium and germanium, China banned the export of antimony-containing products to the US in 2024. China accounts for half of the world’s antimony production, widely used in the military industry for ammunition and nuclear weapons manufacturing.

Previously, antimony extraction was considered unprofitable, but by November 2024, the Rotterdam price for antimony reached $39,000 per ton, over three times its price at the start of the year. Canadian company Spearmint Resources announced plans to resume antimony mining in New Brunswick, signalling the potential exploration and development of new antimony deposits globally.

The role of rare earth and minor metals in the global green economy

The global shift towards a ‘green’ economy has been a key factor driving up the prices of rare earth and minor metals. Countries aim to reduce carbon emissions and adopt renewable energy sources, significantly increasing demand for metals needed to produce solar panels, wind turbines, and batteries. Additionally, the rapid development of electric vehicles (EVs) requires large quantities of lithium, cobalt, nickel, and other rare earth elements for batteries and electric motors. Limited supplies, concentrated in a few countries like China, and the high costs of environmentally safe extraction have further pushed up prices. Moreover, these materials’ critical role in future technologies has spurred speculative market growth. As a result, the costs of rare and minor metals, central to the ‘green’ economy, have risen globally.

Niche markets and pricing for rare commodities Beyond metals widely traded on exchanges, some rare minerals are difficult to price due to infrequent transactions, unique characteristics, and the lack of a standard market. For instance, osmium, especially its isotope osmium-187, is one of the rarest and most unique commodities in the global metal market. Kazakhstan is the primary exporter of osmium-187, making it extremely scarce.

Due to its rarity and specific mining requirements, osmium-187 is not traded on exchanges, and its market price is determined by laboratory assessments of quality, purity, and uniqueness, as well as previous transaction data. This pricing structure highlights the strategic importance of osmium-187 for high-tech and scientific applications, where it remains irreplaceable.

ISE’s metal price database

For over ten years, ISE has maintained its proprietary metal price database, which includes over 19,500 items. This database is built from diverse sources, including insider information about non-exchange-traded metals. Users of the monitoring system include individual clients, major electrical equipment manufacturers, international auditing firms, governmental institutions, and global research universities. Access to the system is available via the ISE AG website on an annual subscription basis, with a 24-hour trial period. Data is updated daily and can be exported in CSV format.

Monitoring metal prices helps identify key drivers of technological progress and their impact on the global economy, as well as anticipate economic changes. This makes it a crucial tool for businesses, policymakers, and researchers alike.

About the Institute for Rare Earth Elements and Metals

The Institute for Rare Earth Elements and Metals AG (ISE AG), established in 2008, is a leading company specialising in high-precision metallurgical analysis and metal storage. Headquartered in Switzerland, the company operates offices in six countries and maintains a global network of 80 employees.

ISE AG focuses on analysing precious and rare earth metals, as well as high-purity industrial products. The company offers highly secure storage facilities in modern warehouses spanning over 8,000m² in Switzerland, ensuring strict inspection and documentation protocols to preserve material integrity.

In its laboratories, ISE AG employs advanced technologies such as GD-MS, ICP-MS, and XRF to perform detailed analyses of a wide range of metals in compliance with ISO standards. Additionally, the company provides metal valuation services, offering reports and audits aligned with IFRS13 standards, and grants online access to real-time prices of over 19,500 metals and their products, enabling informed decisionmaking in a dynamic market environment. ISE AG is also actively involved in research, particularly in the field of metal recycling, collaborating with international universities to develop sustainable methods for recovering critical rare earth elements and minor metals.

Combining cutting-edge technology with a commitment to quality and sustainable resource use, ISE AG is a trusted partner in the metallurgical industry.

kritische Rohstoffe, ISE AG Switzerland, Führung in der Metallindustrie, Experte für seltene Erden, Metallanalyse und Bewertung, Nachhaltige Ressourcennutzung, Internationale Metallmärkte, Metallpreis-Analyse, Metallpreis-Datenbank, High-precision metallurgical analysis, GD-MS, ICP-MS, XRF-Technologien, ISO-konforme Metallanalysen, IFRS13 Metallbewertung, Metallrecycling-Forschung, Nachhaltige Metallrückgewinnung, Metallpreisüberwachungssystem, High-purity industrial metals, Advanced metal analytics, Metalllagerung mit höchster Sicherheit, Seltene Erden und Metalle, Globale Metallpreise, Edelmetallmarkt, Gallium, Germanium, Antimon, Osmium-187, Rohstoffknappheit, Green Economy, Elektrische Fahrzeuge (EV) und Batteriemetalle, Geopolitische Einflüsse auf Metallpreise, Arndt Uhlendorff – Leadership in Rare Earths and Metals, Tracking global metal price trends – ISE AG Switzerland, Innovative metal analysis and storage solutions, Research and sustainability in rare earth elements, Trusted partner for high-precision metal analytics, Metallanalyse Schweiz (metal analysis Switzerland), Hochpräzise Metallanalytik (high-precision metallurgical analysis), Metallbewertung nach IFRS13 (metal valuation IFRS13), Metallpreis-Datenbank (metal price database), Edelmetalllagerung Schweiz (precious metal storage Switzerland), Forschung zu kritischen Rohstoffen (critical raw materials research), Nachhaltige Metallrückgewinnung (sustainable metal recycling), Arndt Uhlendorff CEO ISE AG, Einfluss geopolitischer Ereignisse auf Metallpreise, Gallium, Germanium und Antimon Markttrends, Osmium-187 Marktwert und Anwendungen, Künstliche Intelligenz und Metallnachfrage, Grüne Energie und Rohstoffbedarf, Recycling seltener Erden, Schweizer Labor für Metallanalyse, Sicheres Metalllager für Investoren, Preisentwicklung von Edelmetallen, High-tech metal analytics and sustainability

- Hits: 2068